VAT Calculator

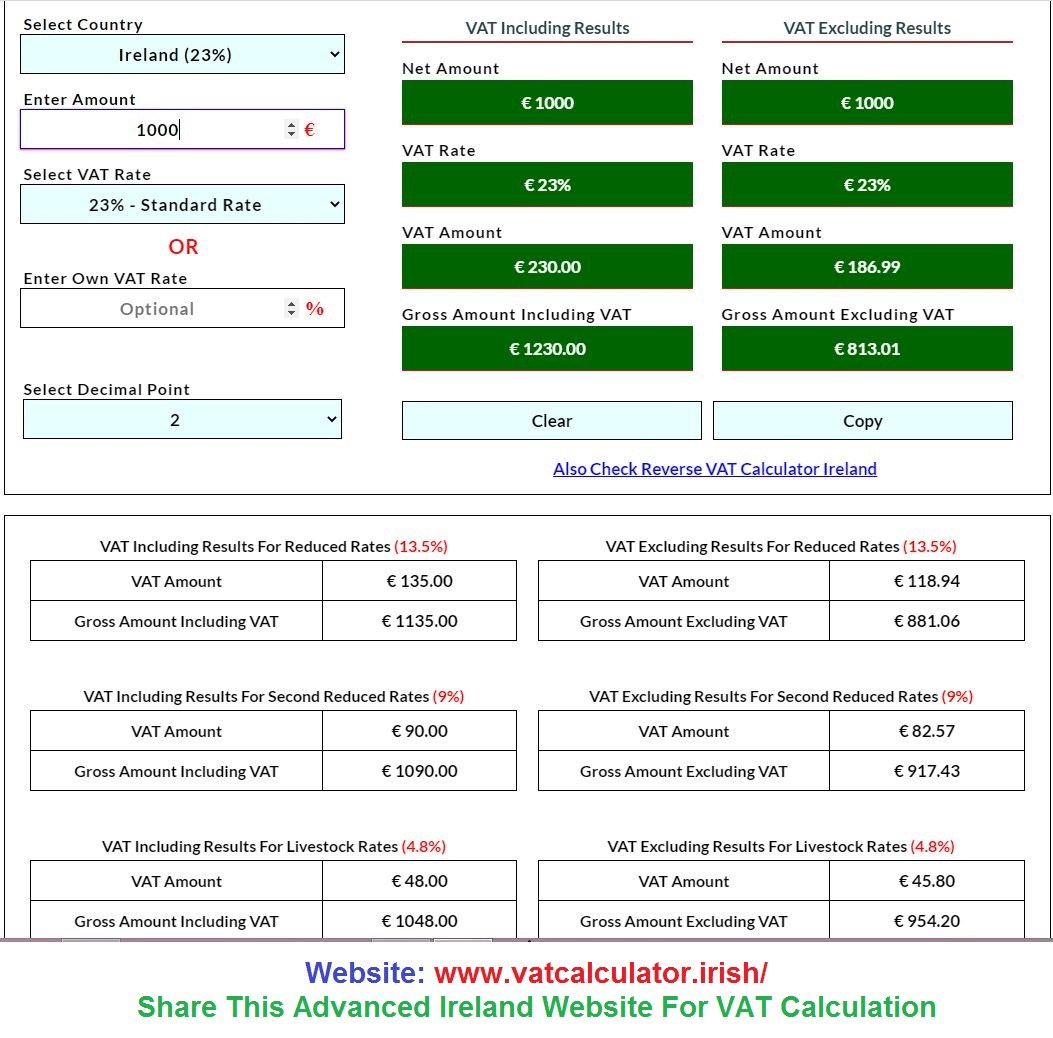

The standard VAT Rate in Ireland Is 23%. But Let's Talk about other VAT Rates in Ireland you may have heard that it's only a 23% VAT Rate In Ireland But Not here we have a lot of Higher VAT Rates in "IE". 13.5% Is the reduced VAT Rate for Ireland 9% is the other VAT Rate in Irish while there are two more VAT Rates in Ireland 5% and 4.8% with their specific criteria and requirements. Now these VAT Rate changes according to the situation all over the world it depending on every country's economic Growth. Here we talking about how to calculate VAT In Ireland there are two ways for VAT Calculation first way is manual with a formula and the second VAT Rate Calculation is with some advanced calculating tool over the internet. So which is the best way to calculate your VAT Accurately without any problem? If you are doing your tax calculation manually then it will take a lot of your time and headache for you to handle it. But on the internet, there are multiple tools where you can calculate your tax accurately and instantly without any problem. The Must use VAT Calculator.

VAT Calculator Ireland is the most perfect and advanced we have seen and found for you because this VAT Calculator Solve your every tax problem they have multiple advanced features like for the same amount you give they generate all the VAT Rates Result of Ireland means if you selected 23% VAT Rate then this tool will give you 23% Result along with Other VAT Rates Result too like for 13.5%, 9%, 5% and 4.8% with the same you gave absolutely fantastic tool for Tax In Ireland. With VAT at 10% (total tax in bold):Each company is responsible for completing the documentation necessary to pass on the VAT collected on its gross margin to the government. Companies are exempt from the requirement to obtain certification from non-end-user buyers and to provide this certification to their suppliers, but they incur higher accounting costs to collect taxes, which are not reimbursed by the Treasury. For example, wholesale businesses now have to hire staff and accountants to handle sales tax paperwork, which wouldn't be necessary if they collected sales tax. VAT, like most taxes, distorts what would have happened without VAT. When the price of a person increases, the quantity of goods traded decreases.

Sales tax or Value-added tax In Ireland

Introduction to the Irish VAT System

Ireland Value-Added Tax (VAT) is an indirect tax, which means it is passed on by business operations to the end consumer. Ireland VAT (Value Added Tax)This tax is charged per stage of production, with businesses re-couping the cost as part of so doing business in Ireland.rThe standard rateis 23%, applying to most goods and servicesReduced rates are700rive for specific sectors:9%, incl uding hospitality13.5%. newspapers4.8%, certain agricultural products0 percent If a €100 meal is served in Dublin by way of example, the VAT rate is 13.5% which means it will include an additional €13.50 making a total bill of €113.50 This layered tax has been implemented to ensure that industries are taxed at rates more suited for what they produce, thus correcting an inherent imbalance in the paradigm of Goods and Services taxation. Businesses pay VAT bit-item and ultimately the cost is borne by the final consumer, highlighting its position as a consumption tax in Ireland's fiscal system.

Value-Added Tax Compliance for Irish Businesses

Irish businesses must register for VAT beyond a certain level of turnover, which are €37,500 (for services) and €75,000 (sales). Compliance includes being able to correctly calculate, collect and pay VAT in full with the Revenue Commissioners of Ireland, while filing periodic VAT returns. Example: The standard rate of VAT applies to a small business in Cork making handmade furniture with an annual turnover of €80,000. For example, if a table costs €500 and the VAT is 20 %, then the consumer will need to pay an additional €115 of taxes which makes it total amount that he or she have to give =€615. He must then pay over that €115 VAT he collected to the Tax man. The system also benefits the exchequer and keeps a level playing field between businesses operating in Ireland, making sure that VAT liabilities are paid across all sectors.

With VAT at 10%. Producers spend ($1 x 1.10) = $1.10 on raw materials and sellers of raw materials pay the government $0.10. The manufacturer charges the retailer ($1.20 × 1.10) = $1.32 and pays the government ($0.12 minus $0.10) = $0.02, leaving a gross margin of ($1 .32 – $1.10 – $0.02) = $0.20. The retailer charges the consumer ($1.50 × 1.10) = $1.65 and pays the government ($0.15 minus $0.12) = $0.03, leaving a gross margin of ($1 .65 – $1.32 – $0.03) = $0.30. Manufacturers and retailers earn lower gross margins in percentage terms. If the production cost of the raw material is specified, this will also apply to the gross margin percentage of the raw material supplier. Please note that the tax paid to the government by manufacturers and retailers is 10% of the value added by their respective business practices (for example, the value added by the manufacturer is $1.20 minus $1.00, the tax payable by the producer is ($1.20) . – $1.00 ) × 10% = $0.02).In the sales tax example above, the consumer pays and the government receives the same amount of sales tax. At each stage of production, the seller collects the tax on behalf of the government, and the buyer pays the tax by paying a higher price. The buyer can then recover the tax payment, but only by successfully selling the value-added product to the buyer or consumer at a later stage. In the example shown above, if the retailer fails to sell some of its stock, it suffers a greater financial loss in the VAT regime, compared to the sales tax regulatory system, because it has paid a higher wholesale price for the products it sells.

As a result, some people are worse off from government benefits than from tax revenues. That is, due to changes in supply and demand, more is lost than gained in terms of the balance sheet. This is known as dead weight loss. If the income lost from the economy is greater than the government's income, the tax is inefficient. VAT and non-VAT have similar implications for microeconomic models. As a consumption tax, VAT is usually used to replace sales tax. Ultimately, it taxes the same people and companies the same amount, even if the inner workings are different. There are significant differences between VAT and sales tax for imported and exported goods:

VAT is charged on exported goods when they are not exported. Sales tax is paid on the full price of imported goods, while VAT can only be charged on the value added to such goods by importers and retailers. This means that without special measures, goods are taxed twice if they are exported from a country that does not charge VAT to another country that charges sales tax. In contrast, goods imported from a VAT-exempt country to another VAT country are subject to no sales tax and only a fraction of the normal VAT. There are also significant differences in the taxation of imported/exported goods between countries with different VAT systems or rates. Sales tax does not have this problem: it is charged the same for both imported and domestic goods and is never charged twice.

To solve this problem, almost all countries that use VAT use special rules for imported and exported goods: All imported goods are subject to VAT at the full price on first sale.

All exported goods are exempt from any VAT payments. The full amount of state revenue (tax revenue) is not required. In Germany, the product is sold to a German retailer for $2500 + VAT ($3000). German retailers request a VAT refund from the

state (refund time varies depending on local and state law) and then charge the VAT to the customer. In the United States, products with exemption certificates are sold to other US retailers for $2,500 (excluding VAT). US retailers charge sales tax to

customers.

Note: The VAT system introduced in Europe affects the cash flow of businesses due to compliance costs and the risk of fraud for governments due to excessive taxation.

For B2B sales between countries it is different: reverse charge applies (no VAT is charged) or sales tax exemption applies. In the case of B2C sales, the seller must pay VAT or sales tax in the consumer's country (creating a controversial situation by

requiring a foreign company to pay its resident/citizen tax which can be taxed without jurisdiction over the seller ).

{kind=link}